import matplotlib.pyplot as plt

import numpy as np

import sympy as sy

import pandas as pd

from scipy.optimize import minimize

Introduction to Linear Regression and Linear Programming#

OBJECTIVES

Derive ordinary least squares models for data

Evaluate regression models using mean squared error

Examine errors and assumptions in least squares models

Use

scikit-learnto fit regression models to dataSet up linear programming problems with constraints using

scipy.optimize

Calculus Refresher#

An important idea is that of finding a maximum or minimum of a function. From calculus, we have the tools required. Specifically, a maximum or minimum value of a function \(f\) occurs wherever \(f'(x) = 0\) or is underfined. Consider the function:

def f(x): return x**2

x = np.linspace(-2, 2, 100)

plt.plot(x, f(x))

plt.grid()

plt.title(r'$f(x) = x^2$');

Here, using our power rule for derivatives of polynomials we have:

and are left to solve:

or

PROBLEM: Use minimize to determine where the function \(f(x) = (5 - 2x)^2\) has a minimum.

def f(x): return (5 - 2*x)**2

x = np.linspace(-2, 5, 100)

plt.plot(x, f(x))

plt.grid();

minimize?

Signature:

minimize(

fun,

x0,

args=(),

method=None,

jac=None,

hess=None,

hessp=None,

bounds=None,

constraints=(),

tol=None,

callback=None,

options=None,

)

Docstring:

Minimization of scalar function of one or more variables.

Parameters

----------

fun : callable

The objective function to be minimized.

``fun(x, *args) -> float``

where ``x`` is a 1-D array with shape (n,) and ``args``

is a tuple of the fixed parameters needed to completely

specify the function.

x0 : ndarray, shape (n,)

Initial guess. Array of real elements of size (n,),

where ``n`` is the number of independent variables.

args : tuple, optional

Extra arguments passed to the objective function and its

derivatives (`fun`, `jac` and `hess` functions).

method : str or callable, optional

Type of solver. Should be one of

- 'Nelder-Mead' :ref:`(see here) <optimize.minimize-neldermead>`

- 'Powell' :ref:`(see here) <optimize.minimize-powell>`

- 'CG' :ref:`(see here) <optimize.minimize-cg>`

- 'BFGS' :ref:`(see here) <optimize.minimize-bfgs>`

- 'Newton-CG' :ref:`(see here) <optimize.minimize-newtoncg>`

- 'L-BFGS-B' :ref:`(see here) <optimize.minimize-lbfgsb>`

- 'TNC' :ref:`(see here) <optimize.minimize-tnc>`

- 'COBYLA' :ref:`(see here) <optimize.minimize-cobyla>`

- 'SLSQP' :ref:`(see here) <optimize.minimize-slsqp>`

- 'trust-constr':ref:`(see here) <optimize.minimize-trustconstr>`

- 'dogleg' :ref:`(see here) <optimize.minimize-dogleg>`

- 'trust-ncg' :ref:`(see here) <optimize.minimize-trustncg>`

- 'trust-exact' :ref:`(see here) <optimize.minimize-trustexact>`

- 'trust-krylov' :ref:`(see here) <optimize.minimize-trustkrylov>`

- custom - a callable object, see below for description.

If not given, chosen to be one of ``BFGS``, ``L-BFGS-B``, ``SLSQP``,

depending on whether or not the problem has constraints or bounds.

jac : {callable, '2-point', '3-point', 'cs', bool}, optional

Method for computing the gradient vector. Only for CG, BFGS,

Newton-CG, L-BFGS-B, TNC, SLSQP, dogleg, trust-ncg, trust-krylov,

trust-exact and trust-constr.

If it is a callable, it should be a function that returns the gradient

vector:

``jac(x, *args) -> array_like, shape (n,)``

where ``x`` is an array with shape (n,) and ``args`` is a tuple with

the fixed parameters. If `jac` is a Boolean and is True, `fun` is

assumed to return a tuple ``(f, g)`` containing the objective

function and the gradient.

Methods 'Newton-CG', 'trust-ncg', 'dogleg', 'trust-exact', and

'trust-krylov' require that either a callable be supplied, or that

`fun` return the objective and gradient.

If None or False, the gradient will be estimated using 2-point finite

difference estimation with an absolute step size.

Alternatively, the keywords {'2-point', '3-point', 'cs'} can be used

to select a finite difference scheme for numerical estimation of the

gradient with a relative step size. These finite difference schemes

obey any specified `bounds`.

hess : {callable, '2-point', '3-point', 'cs', HessianUpdateStrategy}, optional

Method for computing the Hessian matrix. Only for Newton-CG, dogleg,

trust-ncg, trust-krylov, trust-exact and trust-constr.

If it is callable, it should return the Hessian matrix:

``hess(x, *args) -> {LinearOperator, spmatrix, array}, (n, n)``

where ``x`` is a (n,) ndarray and ``args`` is a tuple with the fixed

parameters.

The keywords {'2-point', '3-point', 'cs'} can also be used to select

a finite difference scheme for numerical estimation of the hessian.

Alternatively, objects implementing the `HessianUpdateStrategy`

interface can be used to approximate the Hessian. Available

quasi-Newton methods implementing this interface are:

- `BFGS`;

- `SR1`.

Not all of the options are available for each of the methods; for

availability refer to the notes.

hessp : callable, optional

Hessian of objective function times an arbitrary vector p. Only for

Newton-CG, trust-ncg, trust-krylov, trust-constr.

Only one of `hessp` or `hess` needs to be given. If `hess` is

provided, then `hessp` will be ignored. `hessp` must compute the

Hessian times an arbitrary vector:

``hessp(x, p, *args) -> ndarray shape (n,)``

where ``x`` is a (n,) ndarray, ``p`` is an arbitrary vector with

dimension (n,) and ``args`` is a tuple with the fixed

parameters.

bounds : sequence or `Bounds`, optional

Bounds on variables for Nelder-Mead, L-BFGS-B, TNC, SLSQP, Powell,

trust-constr, and COBYLA methods. There are two ways to specify the

bounds:

1. Instance of `Bounds` class.

2. Sequence of ``(min, max)`` pairs for each element in `x`. None

is used to specify no bound.

constraints : {Constraint, dict} or List of {Constraint, dict}, optional

Constraints definition. Only for COBYLA, SLSQP and trust-constr.

Constraints for 'trust-constr' are defined as a single object or a

list of objects specifying constraints to the optimization problem.

Available constraints are:

- `LinearConstraint`

- `NonlinearConstraint`

Constraints for COBYLA, SLSQP are defined as a list of dictionaries.

Each dictionary with fields:

type : str

Constraint type: 'eq' for equality, 'ineq' for inequality.

fun : callable

The function defining the constraint.

jac : callable, optional

The Jacobian of `fun` (only for SLSQP).

args : sequence, optional

Extra arguments to be passed to the function and Jacobian.

Equality constraint means that the constraint function result is to

be zero whereas inequality means that it is to be non-negative.

Note that COBYLA only supports inequality constraints.

tol : float, optional

Tolerance for termination. When `tol` is specified, the selected

minimization algorithm sets some relevant solver-specific tolerance(s)

equal to `tol`. For detailed control, use solver-specific

options.

options : dict, optional

A dictionary of solver options. All methods except `TNC` accept the

following generic options:

maxiter : int

Maximum number of iterations to perform. Depending on the

method each iteration may use several function evaluations.

For `TNC` use `maxfun` instead of `maxiter`.

disp : bool

Set to True to print convergence messages.

For method-specific options, see :func:`show_options()`.

callback : callable, optional

A callable called after each iteration.

All methods except TNC, SLSQP, and COBYLA support a callable with

the signature:

``callback(OptimizeResult: intermediate_result)``

where ``intermediate_result`` is a keyword parameter containing an

`OptimizeResult` with attributes ``x`` and ``fun``, the present values

of the parameter vector and objective function. Note that the name

of the parameter must be ``intermediate_result`` for the callback

to be passed an `OptimizeResult`. These methods will also terminate if

the callback raises ``StopIteration``.

All methods except trust-constr (also) support a signature like:

``callback(xk)``

where ``xk`` is the current parameter vector.

Introspection is used to determine which of the signatures above to

invoke.

Returns

-------

res : OptimizeResult

The optimization result represented as a ``OptimizeResult`` object.

Important attributes are: ``x`` the solution array, ``success`` a

Boolean flag indicating if the optimizer exited successfully and

``message`` which describes the cause of the termination. See

`OptimizeResult` for a description of other attributes.

See also

--------

minimize_scalar : Interface to minimization algorithms for scalar

univariate functions

show_options : Additional options accepted by the solvers

Notes

-----

This section describes the available solvers that can be selected by the

'method' parameter. The default method is *BFGS*.

**Unconstrained minimization**

Method :ref:`CG <optimize.minimize-cg>` uses a nonlinear conjugate

gradient algorithm by Polak and Ribiere, a variant of the

Fletcher-Reeves method described in [5]_ pp.120-122. Only the

first derivatives are used.

Method :ref:`BFGS <optimize.minimize-bfgs>` uses the quasi-Newton

method of Broyden, Fletcher, Goldfarb, and Shanno (BFGS) [5]_

pp. 136. It uses the first derivatives only. BFGS has proven good

performance even for non-smooth optimizations. This method also

returns an approximation of the Hessian inverse, stored as

`hess_inv` in the OptimizeResult object.

Method :ref:`Newton-CG <optimize.minimize-newtoncg>` uses a

Newton-CG algorithm [5]_ pp. 168 (also known as the truncated

Newton method). It uses a CG method to the compute the search

direction. See also *TNC* method for a box-constrained

minimization with a similar algorithm. Suitable for large-scale

problems.

Method :ref:`dogleg <optimize.minimize-dogleg>` uses the dog-leg

trust-region algorithm [5]_ for unconstrained minimization. This

algorithm requires the gradient and Hessian; furthermore the

Hessian is required to be positive definite.

Method :ref:`trust-ncg <optimize.minimize-trustncg>` uses the

Newton conjugate gradient trust-region algorithm [5]_ for

unconstrained minimization. This algorithm requires the gradient

and either the Hessian or a function that computes the product of

the Hessian with a given vector. Suitable for large-scale problems.

Method :ref:`trust-krylov <optimize.minimize-trustkrylov>` uses

the Newton GLTR trust-region algorithm [14]_, [15]_ for unconstrained

minimization. This algorithm requires the gradient

and either the Hessian or a function that computes the product of

the Hessian with a given vector. Suitable for large-scale problems.

On indefinite problems it requires usually less iterations than the

`trust-ncg` method and is recommended for medium and large-scale problems.

Method :ref:`trust-exact <optimize.minimize-trustexact>`

is a trust-region method for unconstrained minimization in which

quadratic subproblems are solved almost exactly [13]_. This

algorithm requires the gradient and the Hessian (which is

*not* required to be positive definite). It is, in many

situations, the Newton method to converge in fewer iterations

and the most recommended for small and medium-size problems.

**Bound-Constrained minimization**

Method :ref:`Nelder-Mead <optimize.minimize-neldermead>` uses the

Simplex algorithm [1]_, [2]_. This algorithm is robust in many

applications. However, if numerical computation of derivative can be

trusted, other algorithms using the first and/or second derivatives

information might be preferred for their better performance in

general.

Method :ref:`L-BFGS-B <optimize.minimize-lbfgsb>` uses the L-BFGS-B

algorithm [6]_, [7]_ for bound constrained minimization.

Method :ref:`Powell <optimize.minimize-powell>` is a modification

of Powell's method [3]_, [4]_ which is a conjugate direction

method. It performs sequential one-dimensional minimizations along

each vector of the directions set (`direc` field in `options` and

`info`), which is updated at each iteration of the main

minimization loop. The function need not be differentiable, and no

derivatives are taken. If bounds are not provided, then an

unbounded line search will be used. If bounds are provided and

the initial guess is within the bounds, then every function

evaluation throughout the minimization procedure will be within

the bounds. If bounds are provided, the initial guess is outside

the bounds, and `direc` is full rank (default has full rank), then

some function evaluations during the first iteration may be

outside the bounds, but every function evaluation after the first

iteration will be within the bounds. If `direc` is not full rank,

then some parameters may not be optimized and the solution is not

guaranteed to be within the bounds.

Method :ref:`TNC <optimize.minimize-tnc>` uses a truncated Newton

algorithm [5]_, [8]_ to minimize a function with variables subject

to bounds. This algorithm uses gradient information; it is also

called Newton Conjugate-Gradient. It differs from the *Newton-CG*

method described above as it wraps a C implementation and allows

each variable to be given upper and lower bounds.

**Constrained Minimization**

Method :ref:`COBYLA <optimize.minimize-cobyla>` uses the

Constrained Optimization BY Linear Approximation (COBYLA) method

[9]_, [10]_, [11]_. The algorithm is based on linear

approximations to the objective function and each constraint. The

method wraps a FORTRAN implementation of the algorithm. The

constraints functions 'fun' may return either a single number

or an array or list of numbers.

Method :ref:`SLSQP <optimize.minimize-slsqp>` uses Sequential

Least SQuares Programming to minimize a function of several

variables with any combination of bounds, equality and inequality

constraints. The method wraps the SLSQP Optimization subroutine

originally implemented by Dieter Kraft [12]_. Note that the

wrapper handles infinite values in bounds by converting them into

large floating values.

Method :ref:`trust-constr <optimize.minimize-trustconstr>` is a

trust-region algorithm for constrained optimization. It swiches

between two implementations depending on the problem definition.

It is the most versatile constrained minimization algorithm

implemented in SciPy and the most appropriate for large-scale problems.

For equality constrained problems it is an implementation of Byrd-Omojokun

Trust-Region SQP method described in [17]_ and in [5]_, p. 549. When

inequality constraints are imposed as well, it swiches to the trust-region

interior point method described in [16]_. This interior point algorithm,

in turn, solves inequality constraints by introducing slack variables

and solving a sequence of equality-constrained barrier problems

for progressively smaller values of the barrier parameter.

The previously described equality constrained SQP method is

used to solve the subproblems with increasing levels of accuracy

as the iterate gets closer to a solution.

**Finite-Difference Options**

For Method :ref:`trust-constr <optimize.minimize-trustconstr>`

the gradient and the Hessian may be approximated using

three finite-difference schemes: {'2-point', '3-point', 'cs'}.

The scheme 'cs' is, potentially, the most accurate but it

requires the function to correctly handle complex inputs and to

be differentiable in the complex plane. The scheme '3-point' is more

accurate than '2-point' but requires twice as many operations. If the

gradient is estimated via finite-differences the Hessian must be

estimated using one of the quasi-Newton strategies.

**Method specific options for the** `hess` **keyword**

+--------------+------+----------+-------------------------+-----+

| method/Hess | None | callable | '2-point/'3-point'/'cs' | HUS |

+==============+======+==========+=========================+=====+

| Newton-CG | x | (n, n) | x | x |

| | | LO | | |

+--------------+------+----------+-------------------------+-----+

| dogleg | | (n, n) | | |

+--------------+------+----------+-------------------------+-----+

| trust-ncg | | (n, n) | x | x |

+--------------+------+----------+-------------------------+-----+

| trust-krylov | | (n, n) | x | x |

+--------------+------+----------+-------------------------+-----+

| trust-exact | | (n, n) | | |

+--------------+------+----------+-------------------------+-----+

| trust-constr | x | (n, n) | x | x |

| | | LO | | |

| | | sp | | |

+--------------+------+----------+-------------------------+-----+

where LO=LinearOperator, sp=Sparse matrix, HUS=HessianUpdateStrategy

**Custom minimizers**

It may be useful to pass a custom minimization method, for example

when using a frontend to this method such as `scipy.optimize.basinhopping`

or a different library. You can simply pass a callable as the ``method``

parameter.

The callable is called as ``method(fun, x0, args, **kwargs, **options)``

where ``kwargs`` corresponds to any other parameters passed to `minimize`

(such as `callback`, `hess`, etc.), except the `options` dict, which has

its contents also passed as `method` parameters pair by pair. Also, if

`jac` has been passed as a bool type, `jac` and `fun` are mangled so that

`fun` returns just the function values and `jac` is converted to a function

returning the Jacobian. The method shall return an `OptimizeResult`

object.

The provided `method` callable must be able to accept (and possibly ignore)

arbitrary parameters; the set of parameters accepted by `minimize` may

expand in future versions and then these parameters will be passed to

the method. You can find an example in the scipy.optimize tutorial.

References

----------

.. [1] Nelder, J A, and R Mead. 1965. A Simplex Method for Function

Minimization. The Computer Journal 7: 308-13.

.. [2] Wright M H. 1996. Direct search methods: Once scorned, now

respectable, in Numerical Analysis 1995: Proceedings of the 1995

Dundee Biennial Conference in Numerical Analysis (Eds. D F

Griffiths and G A Watson). Addison Wesley Longman, Harlow, UK.

191-208.

.. [3] Powell, M J D. 1964. An efficient method for finding the minimum of

a function of several variables without calculating derivatives. The

Computer Journal 7: 155-162.

.. [4] Press W, S A Teukolsky, W T Vetterling and B P Flannery.

Numerical Recipes (any edition), Cambridge University Press.

.. [5] Nocedal, J, and S J Wright. 2006. Numerical Optimization.

Springer New York.

.. [6] Byrd, R H and P Lu and J. Nocedal. 1995. A Limited Memory

Algorithm for Bound Constrained Optimization. SIAM Journal on

Scientific and Statistical Computing 16 (5): 1190-1208.

.. [7] Zhu, C and R H Byrd and J Nocedal. 1997. L-BFGS-B: Algorithm

778: L-BFGS-B, FORTRAN routines for large scale bound constrained

optimization. ACM Transactions on Mathematical Software 23 (4):

550-560.

.. [8] Nash, S G. Newton-Type Minimization Via the Lanczos Method.

1984. SIAM Journal of Numerical Analysis 21: 770-778.

.. [9] Powell, M J D. A direct search optimization method that models

the objective and constraint functions by linear interpolation.

1994. Advances in Optimization and Numerical Analysis, eds. S. Gomez

and J-P Hennart, Kluwer Academic (Dordrecht), 51-67.

.. [10] Powell M J D. Direct search algorithms for optimization

calculations. 1998. Acta Numerica 7: 287-336.

.. [11] Powell M J D. A view of algorithms for optimization without

derivatives. 2007.Cambridge University Technical Report DAMTP

2007/NA03

.. [12] Kraft, D. A software package for sequential quadratic

programming. 1988. Tech. Rep. DFVLR-FB 88-28, DLR German Aerospace

Center -- Institute for Flight Mechanics, Koln, Germany.

.. [13] Conn, A. R., Gould, N. I., and Toint, P. L.

Trust region methods. 2000. Siam. pp. 169-200.

.. [14] F. Lenders, C. Kirches, A. Potschka: "trlib: A vector-free

implementation of the GLTR method for iterative solution of

the trust region problem", :arxiv:`1611.04718`

.. [15] N. Gould, S. Lucidi, M. Roma, P. Toint: "Solving the

Trust-Region Subproblem using the Lanczos Method",

SIAM J. Optim., 9(2), 504--525, (1999).

.. [16] Byrd, Richard H., Mary E. Hribar, and Jorge Nocedal. 1999.

An interior point algorithm for large-scale nonlinear programming.

SIAM Journal on Optimization 9.4: 877-900.

.. [17] Lalee, Marucha, Jorge Nocedal, and Todd Plantega. 1998. On the

implementation of an algorithm for large-scale equality constrained

optimization. SIAM Journal on Optimization 8.3: 682-706.

Examples

--------

Let us consider the problem of minimizing the Rosenbrock function. This

function (and its respective derivatives) is implemented in `rosen`

(resp. `rosen_der`, `rosen_hess`) in the `scipy.optimize`.

>>> from scipy.optimize import minimize, rosen, rosen_der

A simple application of the *Nelder-Mead* method is:

>>> x0 = [1.3, 0.7, 0.8, 1.9, 1.2]

>>> res = minimize(rosen, x0, method='Nelder-Mead', tol=1e-6)

>>> res.x

array([ 1., 1., 1., 1., 1.])

Now using the *BFGS* algorithm, using the first derivative and a few

options:

>>> res = minimize(rosen, x0, method='BFGS', jac=rosen_der,

... options={'gtol': 1e-6, 'disp': True})

Optimization terminated successfully.

Current function value: 0.000000

Iterations: 26

Function evaluations: 31

Gradient evaluations: 31

>>> res.x

array([ 1., 1., 1., 1., 1.])

>>> print(res.message)

Optimization terminated successfully.

>>> res.hess_inv

array([[ 0.00749589, 0.01255155, 0.02396251, 0.04750988, 0.09495377], # may vary

[ 0.01255155, 0.02510441, 0.04794055, 0.09502834, 0.18996269],

[ 0.02396251, 0.04794055, 0.09631614, 0.19092151, 0.38165151],

[ 0.04750988, 0.09502834, 0.19092151, 0.38341252, 0.7664427 ],

[ 0.09495377, 0.18996269, 0.38165151, 0.7664427, 1.53713523]])

Next, consider a minimization problem with several constraints (namely

Example 16.4 from [5]_). The objective function is:

>>> fun = lambda x: (x[0] - 1)**2 + (x[1] - 2.5)**2

There are three constraints defined as:

>>> cons = ({'type': 'ineq', 'fun': lambda x: x[0] - 2 * x[1] + 2},

... {'type': 'ineq', 'fun': lambda x: -x[0] - 2 * x[1] + 6},

... {'type': 'ineq', 'fun': lambda x: -x[0] + 2 * x[1] + 2})

And variables must be positive, hence the following bounds:

>>> bnds = ((0, None), (0, None))

The optimization problem is solved using the SLSQP method as:

>>> res = minimize(fun, (2, 0), method='SLSQP', bounds=bnds,

... constraints=cons)

It should converge to the theoretical solution (1.4 ,1.7).

File: /Library/Frameworks/Python.framework/Versions/3.12/lib/python3.12/site-packages/scipy/optimize/_minimize.py

Type: function

x0 = 0

results = minimize(fun = f, x0 = x0)

print(results.x)

[2.49999999]

Using the chain rule#

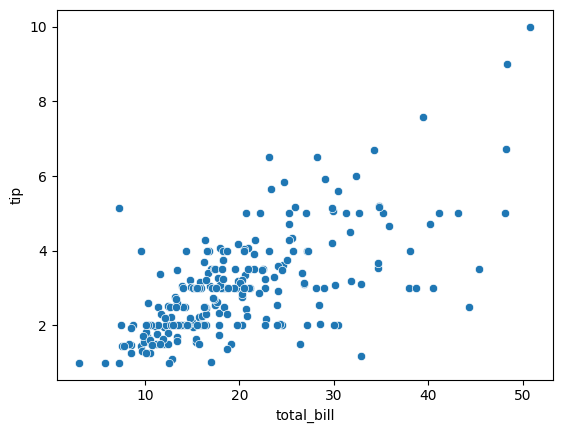

Example 1: Line of best fit

import seaborn as sns

tips = sns.load_dataset('tips')

tips.head()

| total_bill | tip | sex | smoker | day | time | size | |

|---|---|---|---|---|---|---|---|

| 0 | 16.99 | 1.01 | Female | No | Sun | Dinner | 2 |

| 1 | 10.34 | 1.66 | Male | No | Sun | Dinner | 3 |

| 2 | 21.01 | 3.50 | Male | No | Sun | Dinner | 3 |

| 3 | 23.68 | 3.31 | Male | No | Sun | Dinner | 2 |

| 4 | 24.59 | 3.61 | Female | No | Sun | Dinner | 4 |

sns.scatterplot(data = tips, x = 'total_bill', y = 'tip');

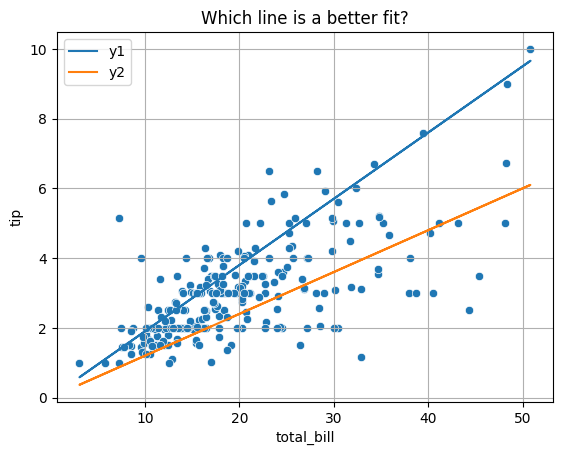

def y1(x): return .19*x

def y2(x): return .12*x

x = tips['total_bill']

plt.plot(x, y1(x), label = 'y1')

plt.plot(x, y2(x), label = 'y2')

plt.legend()

sns.scatterplot(data = tips, x = 'total_bill', y = 'tip')

plt.title('Which line is a better fit?')

plt.grid();

To decide between all possible lines we will examine the error in all these models and select the one that minimizes this error.

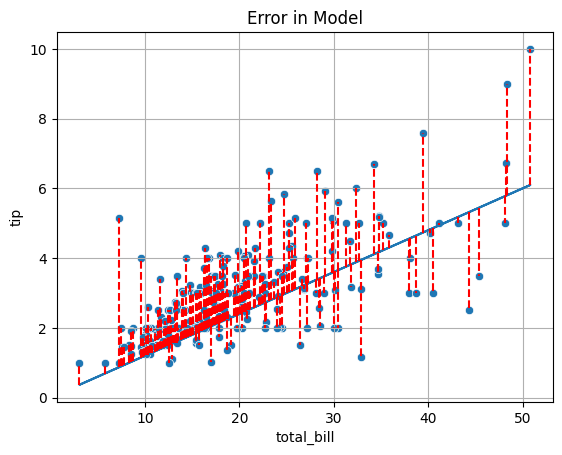

plt.plot(x, y2(x))

for i, yhat in enumerate(y2(x)):

plt.vlines(x = tips['total_bill'].iloc[i], ymin = yhat, ymax = tips['tip'].iloc[i], color = 'red', linestyle = '--')

sns.scatterplot(data = tips, x = 'total_bill', y = 'tip')

plt.title('Error in Model')

plt.grid();

Mean Squared Error#

OBJECTIVE: Minimize mean squared error

def mse(beta):

return np.mean((y - beta*x)**2)

x = tips['total_bill']

y = tips['tip']

mse(.19)

2.185143996844262

mse(.12)

1.4430533029508197

PROBLEM

Use the array of slopes below to loop over each possible slope and determine which gives the lowest Mean Squared Error.

slopes = np.linspace(.1, .2, 11)

slopes

array([0.1 , 0.11, 0.12, 0.13, 0.14, 0.15, 0.16, 0.17, 0.18, 0.19, 0.2 ])

for slope in slopes:

print(slope, mse(slope))

0.1 2.0777683729508194

0.11 1.7133696722540983

0.12000000000000001 1.4430533029508195

0.13 1.2668192650409837

0.14 1.18466755852459

0.15000000000000002 1.1965981834016395

0.16 1.3026111396721312

0.17 1.502706427336066

0.18 1.7968840463934426

0.19 2.185143996844262

0.2 2.667486278688525

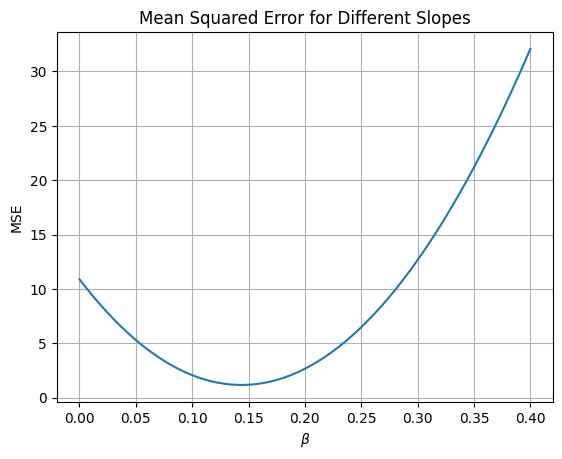

betas = np.linspace(0, .4, 100)

plt.plot(betas, [mse(beta) for beta in betas])

plt.xlabel(r'$\beta$')

plt.ylabel('MSE')

plt.title('Mean Squared Error for Different Slopes')

plt.grid();

Using scipy#

To find the minimum of our objective function, the minimize function can again be used. It requires a function to be minimized and an intial guess.

minimize(mse, x0 = .1)

message: Optimization terminated successfully.

success: True

status: 0

fun: 1.1781161154513358

x: [ 1.437e-01]

nit: 1

jac: [ 1.103e-06]

hess_inv: [[1]]

nfev: 6

njev: 3

Solving the Problem Exactly#

From calculus we know that the minimum value for a quadratic will occur where the first derivative equals zero. Thus, to determine the equations for the line of best fit, we minimize the MSE function with respect to \(\beta\).

np.sum(tips['total_bill']*tips['tip'])/np.sum(tips['total_bill']**2)

0.14373189527721666

Adding an intercept#

Consider the model:

where \(\epsilon = N(0, 1)\).

Now, the objective function changes to be a function in 3-Dimensions where the slope and intercept terms are input and mean squared error is the output.

def mse(betas):

return np.mean((y - (betas[0] + betas[1]*x))**2)

mse([4, 3])

4305.7986356557385

slopes = np.linspace(4, 5, 10)

intercepts = np.linspace(2, 3, 10)

for slope in slopes:

for intercept in intercepts:

print(f'Slope {slope: .2f}, Intercept: {intercept: .2f}, MSE: {mse([slope, intercept])}')

Slope 4.00, Intercept: 2.00, MSE: 1930.6791278688527

Slope 4.00, Intercept: 2.11, MSE: 2148.120884836066

Slope 4.00, Intercept: 2.22, MSE: 2377.1777444444447

Slope 4.00, Intercept: 2.33, MSE: 2617.8497066939894

Slope 4.00, Intercept: 2.44, MSE: 2870.1367715846995

Slope 4.00, Intercept: 2.56, MSE: 3134.038939116575

Slope 4.00, Intercept: 2.67, MSE: 3409.556209289617

Slope 4.00, Intercept: 2.78, MSE: 3696.6885821038245

Slope 4.00, Intercept: 2.89, MSE: 3995.436057559198

Slope 4.00, Intercept: 3.00, MSE: 4305.7986356557385

Slope 4.11, Intercept: 2.00, MSE: 1939.7078305606155

Slope 4.11, Intercept: 2.11, MSE: 2157.6381293209874

Slope 4.11, Intercept: 2.22, MSE: 2387.183530722526

Slope 4.11, Intercept: 2.33, MSE: 2628.3440347652295

Slope 4.11, Intercept: 2.44, MSE: 2881.1196414491

Slope 4.11, Intercept: 2.56, MSE: 3145.510350774134

Slope 4.11, Intercept: 2.67, MSE: 3421.516162740336

Slope 4.11, Intercept: 2.78, MSE: 3709.137077347703

Slope 4.11, Intercept: 2.89, MSE: 4008.373094596235

Slope 4.11, Intercept: 3.00, MSE: 4319.224214485935

Slope 4.22, Intercept: 2.00, MSE: 1948.7612246104027

Slope 4.22, Intercept: 2.11, MSE: 2167.180065163935

Slope 4.22, Intercept: 2.22, MSE: 2397.214008358632

Slope 4.22, Intercept: 2.33, MSE: 2638.8630541944963

Slope 4.22, Intercept: 2.44, MSE: 2892.127202671524

Slope 4.22, Intercept: 2.56, MSE: 3157.006453789719

Slope 4.22, Intercept: 2.67, MSE: 3433.500807549079

Slope 4.22, Intercept: 2.78, MSE: 3721.6102639496057

Slope 4.22, Intercept: 2.89, MSE: 4021.334822991298

Slope 4.22, Intercept: 3.00, MSE: 4332.674484674156

Slope 4.33, Intercept: 2.00, MSE: 1957.839310018215

Slope 4.33, Intercept: 2.11, MSE: 2176.746692364906

Slope 4.33, Intercept: 2.22, MSE: 2407.269177352763

Slope 4.33, Intercept: 2.33, MSE: 2649.4067649817853

Slope 4.33, Intercept: 2.44, MSE: 2903.1594552519737

Slope 4.33, Intercept: 2.56, MSE: 3168.527248163327

Slope 4.33, Intercept: 2.67, MSE: 3445.5101437158464

Slope 4.33, Intercept: 2.78, MSE: 3734.1081419095317

Slope 4.33, Intercept: 2.89, MSE: 4034.3212427443837

Slope 4.33, Intercept: 3.00, MSE: 4346.149446220401

Slope 4.44, Intercept: 2.00, MSE: 1966.9420867840518

Slope 4.44, Intercept: 2.11, MSE: 2186.3380109239015

Slope 4.44, Intercept: 2.22, MSE: 2417.349037704918

Slope 4.44, Intercept: 2.33, MSE: 2659.9751671271

Slope 4.44, Intercept: 2.44, MSE: 2914.216399190447

Slope 4.44, Intercept: 2.56, MSE: 3180.07273389496

Slope 4.44, Intercept: 2.67, MSE: 3457.5441712406387

Slope 4.44, Intercept: 2.78, MSE: 3746.630711227484

Slope 4.44, Intercept: 2.89, MSE: 4047.3323538554946

Slope 4.44, Intercept: 3.00, MSE: 4359.649099124672

Slope 4.56, Intercept: 2.00, MSE: 1976.0695549079135

Slope 4.56, Intercept: 2.11, MSE: 2195.9540208409226

Slope 4.56, Intercept: 2.22, MSE: 2427.4535894150986

Slope 4.56, Intercept: 2.33, MSE: 2670.568260630439

Slope 4.56, Intercept: 2.44, MSE: 2925.2980344869466

Slope 4.56, Intercept: 2.56, MSE: 3191.6429109846176

Slope 4.56, Intercept: 2.67, MSE: 3469.6028901234567

Slope 4.56, Intercept: 2.78, MSE: 3759.1779719034603

Slope 4.56, Intercept: 2.89, MSE: 4060.36815632463

Slope 4.56, Intercept: 3.00, MSE: 4373.173443386967

Slope 4.67, Intercept: 2.00, MSE: 1985.2217143897997

Slope 4.67, Intercept: 2.11, MSE: 2205.594722115969

Slope 4.67, Intercept: 2.22, MSE: 2437.5828324833033

Slope 4.67, Intercept: 2.33, MSE: 2681.1860454918037

Slope 4.67, Intercept: 2.44, MSE: 2936.4043611414695

Slope 4.67, Intercept: 2.56, MSE: 3203.2377794323006

Slope 4.67, Intercept: 2.67, MSE: 3481.686300364298

Slope 4.67, Intercept: 2.78, MSE: 3771.7499239374615

Slope 4.67, Intercept: 2.89, MSE: 4073.428650151791

Slope 4.67, Intercept: 3.00, MSE: 4386.722479007286

Slope 4.78, Intercept: 2.00, MSE: 1994.3985652297108

Slope 4.78, Intercept: 2.11, MSE: 2215.2601147490386

Slope 4.78, Intercept: 2.22, MSE: 2447.7367669095324

Slope 4.78, Intercept: 2.33, MSE: 2691.828521711192

Slope 4.78, Intercept: 2.44, MSE: 2947.535379154018

Slope 4.78, Intercept: 2.56, MSE: 3214.8573392380076

Slope 4.78, Intercept: 2.67, MSE: 3493.794401963165

Slope 4.78, Intercept: 2.78, MSE: 3784.3465673294872

Slope 4.78, Intercept: 2.89, MSE: 4086.5138353369757

Slope 4.78, Intercept: 3.00, MSE: 4400.29620598563

Slope 4.89, Intercept: 2.00, MSE: 2003.600107427646

Slope 4.89, Intercept: 2.11, MSE: 2224.950198740134

Slope 4.89, Intercept: 2.22, MSE: 2457.9153926937865

Slope 4.89, Intercept: 2.33, MSE: 2702.495689288606

Slope 4.89, Intercept: 2.44, MSE: 2958.69108852459

Slope 4.89, Intercept: 2.56, MSE: 3226.5015904017396

Slope 4.89, Intercept: 2.67, MSE: 3505.927194920056

Slope 4.89, Intercept: 2.78, MSE: 3796.9679020795384

Slope 4.89, Intercept: 2.89, MSE: 4099.6237118801855

Slope 4.89, Intercept: 3.00, MSE: 4413.894624322

Slope 5.00, Intercept: 2.00, MSE: 2012.8263409836065

Slope 5.00, Intercept: 2.11, MSE: 2234.664974089254

Slope 5.00, Intercept: 2.22, MSE: 2468.1187098360656

Slope 5.00, Intercept: 2.33, MSE: 2713.1875482240443

Slope 5.00, Intercept: 2.44, MSE: 2969.871489253188

Slope 5.00, Intercept: 2.56, MSE: 3238.1705329234965

Slope 5.00, Intercept: 2.67, MSE: 3518.0846792349726

Slope 5.00, Intercept: 2.78, MSE: 3809.6139281876135

Slope 5.00, Intercept: 2.89, MSE: 4112.75827978142

Slope 5.00, Intercept: 3.00, MSE: 4427.517734016393

minimize(mse, [5, 3])

message: Optimization terminated successfully.

success: True

status: 0

fun: 1.0360194420115216

x: [ 9.203e-01 1.050e-01]

nit: 5

jac: [-5.960e-08 -8.643e-07]

hess_inv: [[ 2.980e+00 -1.253e-01]

[-1.253e-01 6.334e-03]]

nfev: 18

njev: 6

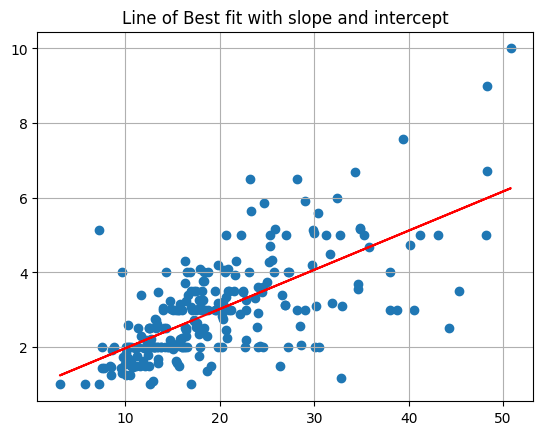

betas = minimize(mse, [0, 0]).x

def lobf(x): return betas[0] + betas[1]*x

plt.scatter(x, y)

plt.plot(x, lobf(x), color = 'red')

plt.grid()

plt.title('Line of Best fit with slope and intercept');

Using scikit-learn#

The scikit-learn library has many predictive models and modeling tools. It is a popular library in industry for Machine Learning tasks. docs

# !pip install -U scikit-learn

credit = pd.read_csv('../data/Credit.csv', index_col=0)

credit.head()

| Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 14.891 | 3606 | 283 | 2 | 34 | 11 | Male | No | Yes | Caucasian | 333 |

| 2 | 106.025 | 6645 | 483 | 3 | 82 | 15 | Female | Yes | Yes | Asian | 903 |

| 3 | 104.593 | 7075 | 514 | 4 | 71 | 11 | Male | No | No | Asian | 580 |

| 4 | 148.924 | 9504 | 681 | 3 | 36 | 11 | Female | No | No | Asian | 964 |

| 5 | 55.882 | 4897 | 357 | 2 | 68 | 16 | Male | No | Yes | Caucasian | 331 |

from sklearn.linear_model import LinearRegression

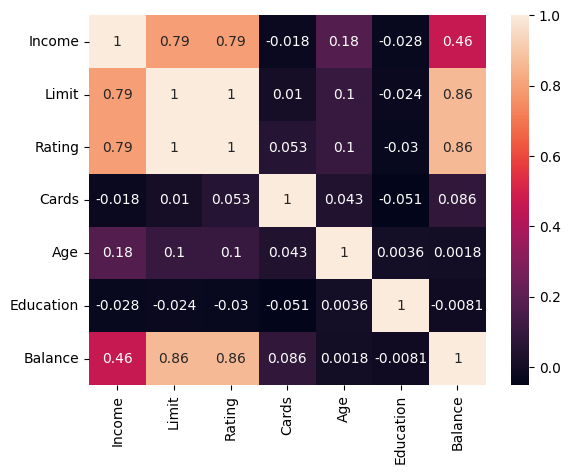

PROBLEM: Which feature is the strongest predictor of Balance in the data?

sns.heatmap(credit.corr(numeric_only = True), annot = True)

<Axes: >

#define X as the feature most correlated with Balance

#and y as Balance

X = credit[['Rating']]

y = credit['Balance']

PROBLEM: Build a LinearRegression model, determine the Root Mean Squared Error and interpret the slope and intercept.

Instantiate

Fit

Predict/score

X.shape, y.shape

((400, 1), (400,))

#instantiate

model = LinearRegression()

#fit

model.fit(X, y)

LinearRegression()In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

LinearRegression()

#look at coefficient and intercept

model.coef_, model.intercept_

(array([2.56624033]), -390.84634178723786)

yhat = model.predict(X)

yhat[:10]

array([ 335.39967085, 848.64773632, 928.20118647, 1356.76332113,

525.30145507, 1069.34440447, 273.80990299, 923.06870581,

291.77358529, 869.17765894])

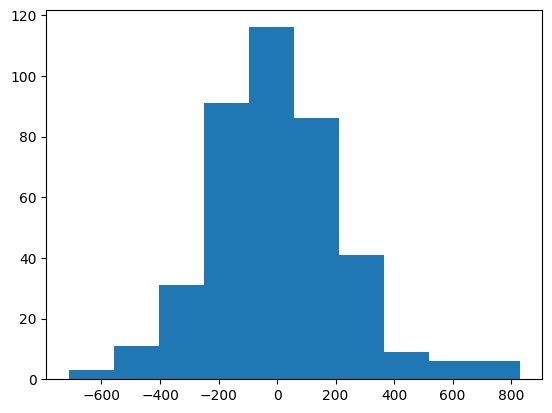

#examine the distribution of errors -- want normal centered at 0

plt.hist((y - yhat))

(array([ 3., 11., 31., 91., 116., 86., 41., 9., 6., 6.]),

array([-712.2825064 , -558.1506416 , -404.01877679, -249.88691199,

-95.75504718, 58.37681762, 212.50868243, 366.64054724,

520.77241204, 674.90427685, 829.03614165]),

<BarContainer object of 10 artists>)

model.score(X, y) #r^2 score

0.7458484180585037

from sklearn.metrics import mean_squared_error

#make predictions

#error between true and predicted

mean_squared_error(y, yhat)

53587.80508183237

np.sqrt(mean_squared_error(y, yhat)) #Root Mean Squared Error

231.4903995457098

credit.head(2)

| Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 14.891 | 3606 | 283 | 2 | 34 | 11 | Male | No | Yes | Caucasian | 333 |

| 2 | 106.025 | 6645 | 483 | 3 | 82 | 15 | Female | Yes | Yes | Asian | 903 |

X2 = credit[['Rating', 'Limit', 'Income', 'Age']]

model2 = LinearRegression()

model2.fit(X2, y)

LinearRegression()In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

LinearRegression()

yhat2 = model2.predict(X2)

np.sqrt(mean_squared_error(y, yhat2))

160.88858783942516

model2.coef_

array([ 2.73142151, 0.08183201, -7.61267561, -0.85611769])

Problem: Determine \(\alpha\) and \(\beta\) of an investment#

Consider an investment with return of the market as \(R_M\) (say the S&P) and the return of a stock \(R\) over the same time period.

import yfinance as yf

data = yf.download(["NVDA", "SPY"], period="5y")

data.head()

data.info()

close = data.iloc[:, [0, 1]]

close.pct_change().plot()

returns = close.pct_change()

sns.regplot(x = returns.iloc[:, 1], y = returns.iloc[:, 0], scatter_kws={'alpha': 0.3})

plt.xlabel('SPY Close Pct Change')

plt.ylabel('NVDA Close Pct Change')

plt.grid();

#instantiate

#fit

#examine our alpha and beta

Problem#

Load in the california housing data from the sample_data folder in colab. Use this data to build a regression model with:

The most correlated feature to housing prices as input and price as target

The five features you believe would be most important

Which model has a lower MSE?

Linear Programming: An example#

A dog daycare feeds the dogs a diet that requires a minimum of 15 grams of fiber, 30 grams of protein. Each pound of chick peas contains 1 gram of protein, 5 grams of fiber, and 25 grams of fat. Cottage cheese contains 2 grams of protein, 1 gram of fiber, and 14 grams of fat. Suppose that chick peas are priced at 8 USD per pound, and cottage cheese at 6 USD per pound. The nutritionist claims the dogs will not eat more than 285 grams of fat. Your goal is to obtain the most economical solution given these constraints.

This is summarized in the table below:

ingredient |

protein |

fiber |

fat |

cost |

|---|---|---|---|---|

chick peas |

1 g |

5 g |

25 g |

$8 |

cottage cheese |

2 g |

1 g |

14 g |

$6 |

minimum |

15 g |

30 g |

||

maximum |

285 g |

Mathematically, the objective function is:

where \(x\) = chick peas and \(y\) = cottage cheese. This is the total cost of the combination of chick peas and cottage cheese.

We will save the coefficients as a list for use later.

c = [6, 8]

Because each pound of chick peas contains 1 gram of protein and each cottage cheese 2 grams, and know this needs to combine to at least 15 grams you have:

As for cottage cheese, you have:

As for the fat content, you have:

Further, the amount of \(x\) and \(y\) must not be negative.

Graphical representation#

To visualize the solution, you can imagine each of the constraints as a region. First, functions for these are defined and plotted together.

def cp(x): #chick peas

return -2*x + 15

def cc(x): #cottage cheese

return -1/5*x + 30/5

def fat(x): #fat

return -14/25*x + 285/25

y = 0

x = np.linspace(0, 30, 100)

d = np.linspace(0, 30, 1000)

x, y = np.meshgrid(d, d)

plt.imshow((y > cp(x)) & (y < fat(x)) & (y > cc(x)).astype('int'),

origin = 'lower',

cmap = 'Greys',

extent=(x.min(), x.max(), y.min(), y.max()),

alpha = 0.4)

plt.plot(d, cc(d), '-', color = 'black', label = 'cottage cheese')

plt.plot(d, cp(d), '-', color = 'blue', label = 'chick peas')

plt.plot(d, fat(d), '-', color = 'red', label = 'fat')

plt.ylim(0, 15)

plt.xlim(0, 20)

plt.title('Feasible region for dog food problem')

plt.grid();

The form of all solutions can be found by rewriting the objective function as:

Below, different values of \(C\) are plotted against the original region. Note that the objective function will obtain its maximum and minimum values at the vertices of the polygon. Hence, to solve the problem, you need only look to the vertices. These are highlighted in the plot on the right.

# fig, ax = plt.subplots(1, 2, figsize = (30, 10))

for i in range(10, 1000, 10):

plt.plot(d, -6/8*d + i/8, '--', color = 'black')

plt.plot(d, -6/8*d + i, '--', color = 'black', label = 'slopes of -6/8 + c/8')

d = np.linspace(0, 30, 1000)

x, y = np.meshgrid(d, d)

plt.imshow((y > cp(x)) & (y < fat(x)) & (y > cc(x)).astype('int'),

origin = 'lower',

cmap = 'Greys',

extent=(x.min(), x.max(), y.min(), y.max()),

alpha = 0.4)

plt.plot(d, cc(d), '-', color = 'black', label = 'cottage cheese')

plt.plot(d, cp(d), '-', color = 'blue', label = 'chick peas')

plt.plot(d, fat(d), '-', color = 'red', label = 'fat')

plt.ylim(0, 15)

plt.xlim(0, 20)

plt.title('Feasible region for dog food problem\nwith possible cost lines')

plt.grid()

plt.legend();

d = np.linspace(0, 30, 1000)

x, y = np.meshgrid(d, d)

plt.imshow((y > cp(x)) & (y < fat(x)) & (y > cc(x)).astype('int'),

origin = 'lower',

cmap = 'Greys',

extent=(x.min(), x.max(), y.min(), y.max()),

alpha = 0.4)

plt.plot(d, cc(d), '-', color = 'black', label = 'cottage cheese')

plt.plot(15, 3, 'ro', label = 'possible solutions')

plt.plot(d, cp(d), '-', color = 'blue', label = 'chick peas')

plt.plot(d, fat(d), '-', color = 'red', label = 'fat')

plt.ylim(0, 15)

plt.xlim(0, 20)

plt.title('Feasible region for dog food problem')

plt.grid()

plt.plot(5, 5, 'ro')

plt.plot(5/2, 10, 'ro')

plt.legend();

using linprog#

To solve the problem using python, scipy.optimize contains the linprog function that will solve this problem. The one exception is that the greater than inequality constraints need to be converted to less thans by multiplying both sides by -1.

#cost coeffients

c = [6, 8]

#coefficients of less than problems

A = [[-2, -1], [-1, -5], [14, 25]]

#right side of inequalities

b = [-15, -30, 285]

res = optim.linprog(c, A, b)

res

EXAMPLE

Suppose we have the opportunity to invest in four projects with given cash flows, net present value, and profitability index (\(\frac{NPV}{\text{investment}}\)) given below.

PROJECT |

\(C_0\) |

\(C_1\) |

\(C_2\) |

NPV at 10% |

Profitability Index |

|---|---|---|---|---|---|

A |

-10 |

-30 |

5 |

21 |

2.1 |

B |

-5 |

5 |

2 |

16 |

3.2 |

C |

-5 |

5 |

15 |

12 |

2.4 |

D |

0 |

-40 |

60 |

13 |

0.4 |

CONSTRAINTS

Cash flows for period 0 must not be greater than 10 million.

Total outflow in period 1 must not be greater than 10 million.

Finally the amount of the investment must be positive and we cannot purchase more than one of each.

from scipy.optimize import linprog

coefs = [-21, -16, -12, -13]

constr = [[10, 5, 5, 0],

[-30, -5, -5, 40]]

right_side = [10, 10]

bounds = [(0, 1), (0, 1), (0, 1), (0, 1)]

linprog(coefs, constr, right_side, bounds = bounds)